Every time things go sideways in the Middle East, the price of gas on the sign at my Petro-Canada jumps ten cents before I’ve finished reading the headline. And every time, the same question pops up in the Tim’s lineup: Why? We’ve got all the oil. We aren’t even buying from those guys.

It’s a fair point. But it misses how the “pool” actually works — and who is really holding the stopwatch.

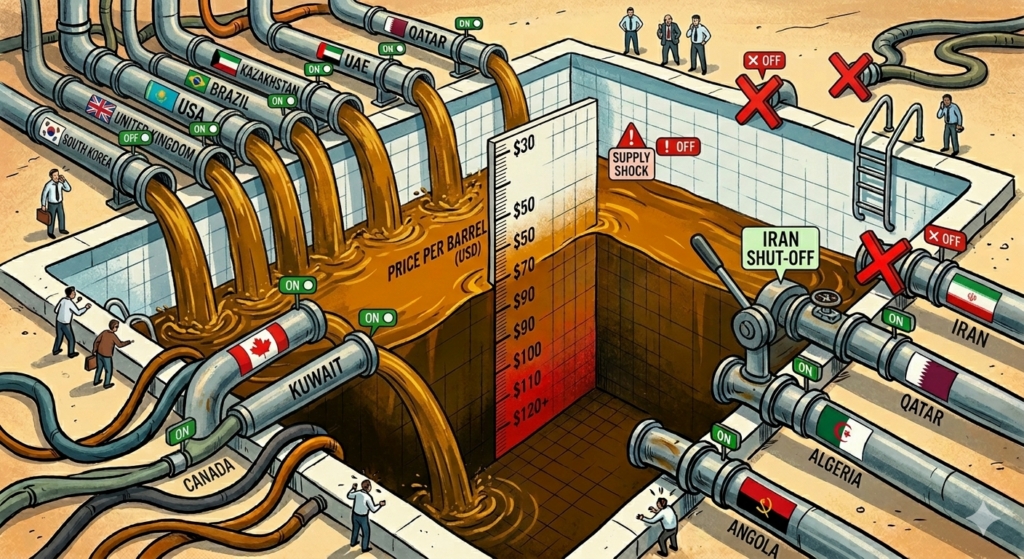

The Giant Swimming Pool

To understand oil, you have to stop thinking about “Canadian oil” or “Saudi oil.” Think of the global market as one massive, Olympic-sized swimming pool.

Every producer — Canada, the U.S., Iraq, Norway — is standing around the edge with a hose, pumping their barrels into that one pool. On the other side, every country that needs fuel draws from it. The price isn’t based on which hose your gas came from; it’s based on how high the water level is in the pool.

The global “level” is a benchmark called Brent Crude. Because we’re plugged into the same pool as everyone else, we pay the pool price. There is no “patriotism discount” just because your barrel came from a well in Saskatchewan.

The Fear Market

Here’s the part most people miss: the price doesn’t wait for a refinery to actually blow up.

Oil is traded on futures markets, meaning traders in London and Houston are buying and selling barrels that haven’t even been pulled out of the ground yet. They aren’t reacting to facts; they’re reacting to risk.

The second a drone flies over a terminal in the Gulf, those traders start pricing in the possibility of a shortage three months from now. The price spikes instantly. Nothing physically changed — no oil was lost — but the risk premium moved, and the global pricing followed. When shipping through the Hormuz becomes uncertain, Brent absorbs that risk immediately. Even markets that aren’t directly exposed, like Canada’s, get pulled along. You can’t opt out of the benchmark just because your barrel came from Saskatchewan.

The Guy at the Gas Station is Just Doing Math

This is why the local station owner changes his sign at 8:00 PM for a war that started at 6:00 PM.

He isn’t charging you based on what he paid for the gas in his tank. He’s charging you based on his replacement cost, which is tied directly to those real-time futures markets. If the global price jumps 15 cents, his next shipment — the one he has to order tomorrow — is going to cost him 15 cents more. If he doesn’t raise his price right now, he won’t have enough cash in the till to buy that next load. He’d go broke just trying to restock. The sign out front isn’t a receipt for the past; it’s a forecast of his next bill.

The Pipeline Trap

“But we’re an oil giant!” people say. “Nearly 6 million barrels a day!”

True. But here’s the kicker: 96% of our exports go straight to the United States through pipelines where we don’t control the pricing. We are a resource superpower with almost zero leverage over what our own resource sells for. We’re hooked into a continental and global grid that tells us what our oil is worth, not the other way around.

Eastern refineries in Quebec and the Maritimes actually import lighter grades of crude because what we pull out of Alberta is mostly heavy oil — not ideal for every refinery. So even domestically, it’s more complicated than “we have oil, we’re fine.”

The 21-Mile Chokepoint

There’s a narrow strip of water between Iran and Oman called the Hormuz. Twenty-one miles wide at its tightest point. Looks like nothing on a map.

In 2024, roughly 20% of everything the planet consumes in oil moved through it every single day. Saudi Arabia, Iraq, the UAE, Kuwait, Qatar — all of them funnelling their exports through this one skinny passage with basically no alternative route if it closes.

And here’s the uncomfortable part: it doesn’t matter that most of that oil is headed to Asia. The moment that supply is threatened, the global price moves. Our price moves with it because our price is the global price.

This isn’t theoretical. In late February 2026, the US and Israel launched military strikes on Iran. Iran hit back across at least nine countries in the Gulf region. The strait effectively closed. Brent crude jumped 10 to 13% in early trading, with serious analysts warning of $100 a barrel if it drags on. That’s the jump showing up at your pump right now.

The Political Noise

We can’t ignore the politics either. When Carney killed the federal carbon tax on his first day as prime minister in March 2025, Canadians felt it immediately. Ontario saw pump prices drop up to 20 cents a litre the morning it took effect. That was a real and direct hit to the cost of living, and it’s worth saying clearly.

But it’s also worth being honest about what’s still there. An industrial carbon price remains on large emitters, and the CTF — a group that has consistently opposed carbon pricing — argues that cost trickles down to roughly seven cents a litre at the pump. That’s a contested number from an advocacy organization, not a neutral source, and you can debate it. But even if you take it at full face value, seven cents doesn’t explain a 13% price spike in a single week.

A 21-mile chokepoint in the Persian Gulf does.

The Bottom Line

The people winning right now aren’t in Ottawa, and they aren’t the guys running the local gas station. They’re the traders playing the futures and the oil majors banking record profits while you do the math on your commute.

We have the oil. We just don’t have any say in what it’s worth. As long as we’re in the pool, we’re at the mercy of whoever is threatening to drain it.